Best Horse Racing Betting Sites – Bet on Horse Racing in 2026

Loading...

You’ve won your bet. The horse crossed the line first, the starting price was right, and the sums looked clean — until the settlement came through and the payout was lower than expected. Somewhere between the final furlong and your account balance, a Rule 4 deduction took a slice. Understanding how that slice is calculated is the difference between a nasty surprise and a number you can see coming.

The calculation itself is not complicated. It’s multiplication, not rocket science. But the inputs matter, and getting them wrong — or confusing which horse’s price drives the deduction — leads to the kind of errors that make punters distrust the system. With average field sizes on the Flat sitting at 8.90 runners per race in 2025 (down from 9.14 the year before, according to the BHA’s 2025 Racing Report), non-runners are a regular feature of the racecard. Plug in the numbers, see what you actually take home.

The Rule 4 Calculation Formula

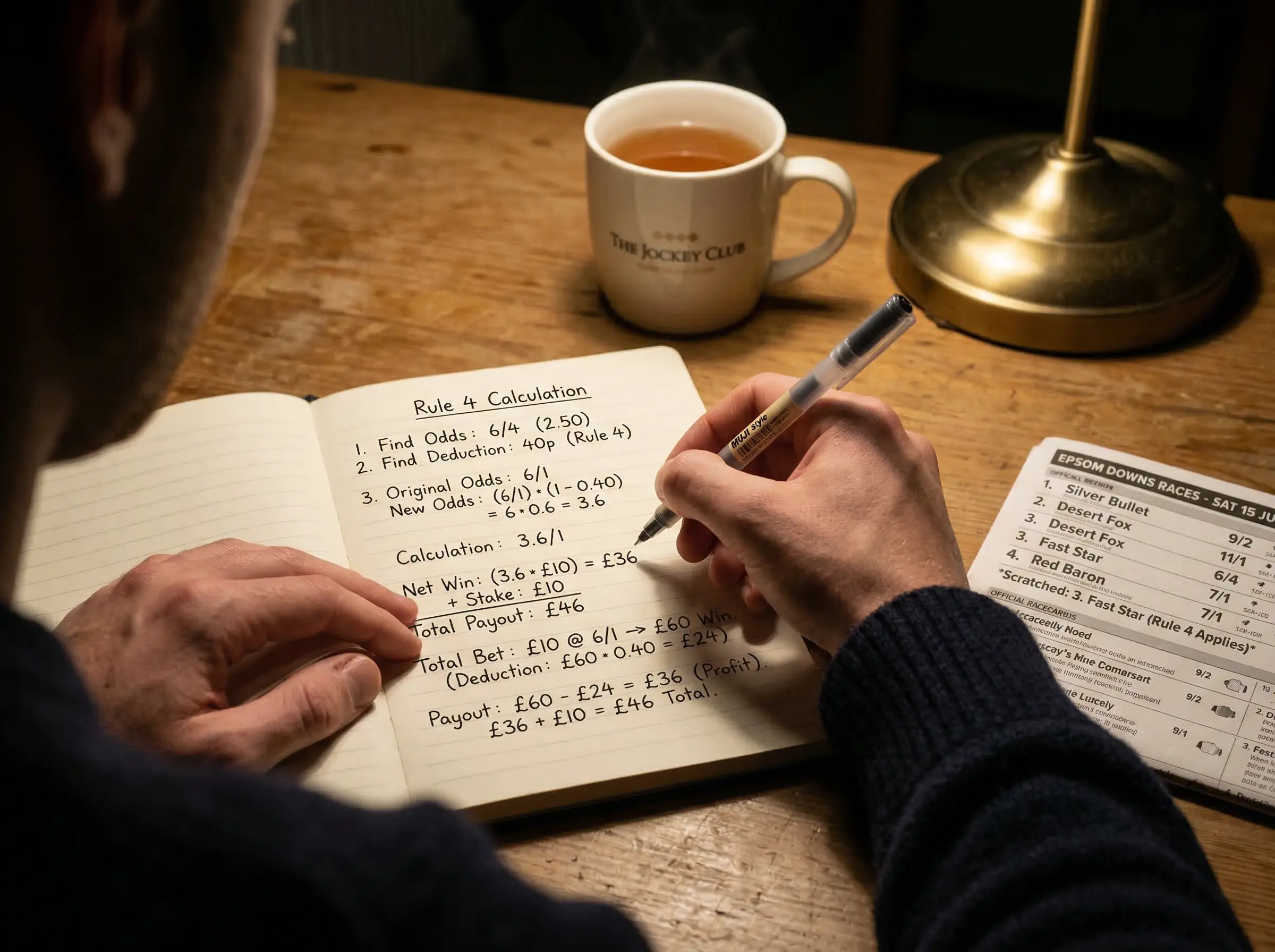

The formula has three steps. First, work out your gross winnings — that’s your stake multiplied by the odds. Second, look up the deduction percentage based on the starting price of the withdrawn horse (not your horse). Third, subtract the deduction from your gross winnings. The result is what lands in your account.

Written out, it looks like this:

Adjusted winnings = Gross winnings − (Gross winnings × Deduction rate)

Or equivalently:

Adjusted winnings = Gross winnings × (1 − Deduction rate)

The deduction rate comes from the Tattersalls Rule 4(c) table, expressed in pence per pound. A 20p deduction means the rate is 0.20. A 45p deduction means 0.45. Your total return is the adjusted winnings plus your original stake, since the stake itself is never subject to Rule 4 — only the winnings are.

One point bears repeating because it’s the source of most confusion: the deduction is determined by the price of the horse that was withdrawn, not the price of your winning horse. If you backed a 10/1 winner and a 2/1 shot was pulled out, the deduction is 30p in the pound — pegged to the 2/1 price, not your 10/1. This catches people out because it feels counterintuitive. But the logic is sound: the withdrawal of a short-priced horse reshapes the market more dramatically, so a larger deduction is applied to compensate.

Example 1: Short-Priced Non-Runner (Evens Favourite)

The market favourite in a seven-runner handicap hurdle is priced at evens (1/1). Half an hour before the off, the trainer withdraws the horse after the going is changed from Good to Soft. Your selection — a 4/1 shot — goes on to win. Here’s what happens to your £20 bet.

Gross winnings: £20 × 4 = £80.

The withdrawn horse was priced at evens. The Rule 4 table assigns a 45p deduction for horses priced between evens and 6/5. That’s a rate of 0.45.

Deduction: £80 × 0.45 = £36.

Adjusted winnings: £80 − £36 = £44.

Total return: £44 (winnings) + £20 (stake) = £64.

Without the non-runner, your return would have been £100. The deduction took £36 — a substantial hit. This is the harsh reality of short-priced non-runners: an evens favourite being withdrawn can take 45% of your winnings in one go. In small fields, where the favourite’s odds are even shorter, the deduction climbs further. At 1/3, you’re looking at a 70p deduction. At 1/9, it’s 90p — leaving you with just 10% of your gross winnings.

Example 2: Long-Priced Non-Runner (10/1 Outsider)

Now take the opposite end of the market. A 10/1 outsider is withdrawn from a twelve-runner Flat handicap after failing a pre-race veterinary inspection. Your selection — a 3/1 joint-favourite — wins. You’ve staked £20.

Gross winnings: £20 × 3 = £60.

The withdrawn horse was priced at 10/1. The table assigns a 5p deduction for horses in the 10/1 to 14/1 range. That’s a rate of 0.05.

Deduction: £60 × 0.05 = £3.

Adjusted winnings: £60 − £3 = £57.

Total return: £57 + £20 = £77.

A £3 deduction on a £60 profit is barely noticeable. This is the normal experience for most punters: the withdrawn horse was an outsider, the market barely flinches, and the deduction is little more than a rounding error. If the withdrawn horse had been priced above 14/1, there would be no deduction at all — the Tattersalls table recognises that removing a long-priced runner has negligible impact on the race’s competitive dynamics.

The contrast between these two examples illustrates the entire philosophy behind Rule 4. It’s a proportional mechanism. The more likely the withdrawn horse was to win, the more the remaining field benefits from its absence, and the larger the adjustment to your payout. A 45p hit from an evens withdrawal and a 5p nick from a 10/1 withdrawal are not the same event, and the deduction table reflects that difference precisely.

Example 3: Two Non-Runners in One Race

Multiple non-runners in a single race aren’t common, but they do happen — particularly on days when the going changes sharply or when a stable illness forces a trainer to pull several entries. When two or more horses are withdrawn, the deductions are cumulative but capped.

Take a ten-runner novice chase. The 5/2 second-favourite and a 7/1 outsider are both withdrawn on the morning of the race. Your selection — priced at 9/2 — wins. You staked £20.

Gross winnings: £20 × 4.5 = £90.

First withdrawal (5/2): the table gives a 25p deduction. Second withdrawal (7/1): the table gives 10p. The cumulative deduction is 25p + 10p = 35p in the pound. That’s well below the 90p maximum, so both deductions apply in full.

Deduction: £90 × 0.35 = £31.50.

Adjusted winnings: £90 − £31.50 = £58.50.

Total return: £58.50 + £20 = £78.50.

Now imagine a more extreme scenario. The 1/2 favourite and the evens second-favourite are both withdrawn from the same race. The individual deductions would be 60p (for the 1/2 shot) and 45p (for the evens horse), totalling 105p. But the maximum cumulative deduction under Tattersalls Rule 4(c) is capped at 90p in the pound. So the combined deduction is 90p, not 105p. On £90 of gross winnings, you’d keep £9 plus your stake — a grim outcome, but at least the cap prevents a total wipeout of your profit.

These multi-withdrawal scenarios are worth understanding even if they’re uncommon. Cheltenham week, Grand National day, and busy Saturday cards at big meetings are the likeliest occasions. When they do occur, plug in the numbers, see what you actually take home — and remember that the cap is your floor, not a target anyone wants to hit.

Run the Numbers Before the Race

The Rule 4 calculation is three steps: work out your gross winnings, look up the deduction for the withdrawn horse’s price, and subtract. That’s it. The maths isn’t the hard part — the hard part is remembering to do it before you assume what your payout should be.

Build the habit of checking for non-runners before each race and noting the prices of any withdrawn horses. If a short-priced runner goes out, you’ll know immediately what it means for your potential return. If a long-priced outsider is pulled, you’ll know the impact is negligible. Either way, the calculation takes thirty seconds and saves you the frustration of a settlement that looks wrong but isn’t. Plug in the numbers, see what you actually take home.